(updated 22nd July 2020)

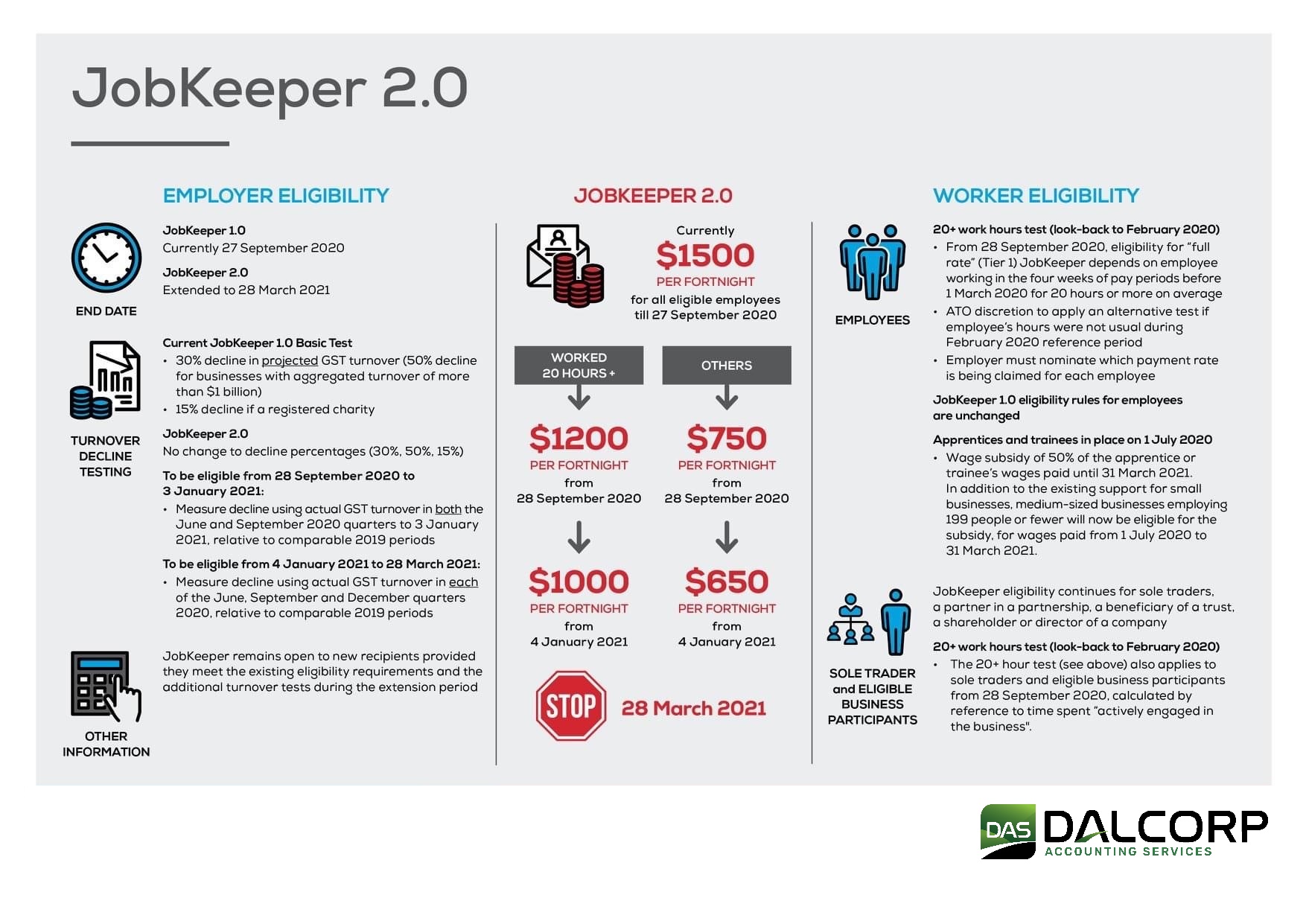

On 21 July, the Government announced it is extending the JobKeeper Payment until 28 March 2021 and is targeting support to those organisations which continue to be significantly impacted by the Coronavirus. From 28 September 2020, eligibility for the JobKeeper Payment will be based on actual turnover in the relevant periods, the payment will be stepped down and paid at two rates.

Who is eligible?

To be eligible for JobKeeper payments under the extension, businesses with an aggregate turnover of $1 billion or less will need to demonstrate that they have experienced a drop in turnover of at least 30 per cent; for those with turnover above this limit, the drop is 50 per cent; and charities are expected to show a 15 per cent shortfall.

But, from 28 September, businesses wanting to remain on JobKeeper will also need to prove they suffered an actual decline in turnover for the June and September quarters.

Subsequently, to keep receiving JobKeeper into 2021, on 4th January businesses will need to reconfirm their turnover shortfall for each of the June, September and December 2020 quarters.

If a business or not-for-profit does not meet the additional turnover tests for the extension period, this does not affect their eligibility prior to 28 September 2020.

The Treasury has also confirmed that the JobKeeper payment will continue to remain open to new recipients, provided they meet the existing eligibility requirements and the additional turnover tests during the extension period.

What are the new amounts?

The JobKeeper payment rate is to be reduced and paid at two rates:

From 28 September 2020 to 3 January 2021, the payment rates will be;

- $1,200 per fortnight for all eligible employees who, in the four weeks before 1 March 2020, were working in the business for 20 hours or more a week on average and for business participants who were actively engaged in the business for more than 20 hours per week, and

- $750 per fortnight for employees who were working in the business for less than 20 hours a week on average and business participants who were actively engaged in the business less than 20 hours per week in the same period.

From 4 January 2021 to 28 March 2021, the payment rate will be;

- $1,000 per fortnight for all eligible employees who in the four weeks before 1 March 2020, were working for 20 hours or more a week on average and for business participants who were actively engaged in the business for more than 20 hours per week, and

- $650 per fortnight for employees who were working for less than 20 hours a week on average and business participants who were actively engaged in the business for less than 20 hours per week in the same period.

The additional turnover test

In order to be eligible for the JobKeeper Payment after 27 September 2020, businesses and not-for-profits will have to meet a further decline in turnover test for each of the two periods of the extension, as well as meeting the other existing eligibility requirements for the JobKeeper Payment.

- In order to be eligible for the first JobKeeper Payment extension period of 28 September 2020 to 3 January 2021, businesses and not-for-profits will need to demonstrate that their actual GST turnover has significantly fallen in the both the June quarter 2020 (April, May and June) and the September quarter 2020 (July, August, September) relative to comparable periods (generally the corresponding quarters in 2019).

- In order to be eligible for the second JobKeeper Payment extension period of 4 January 2021 to 28 March 2021, businesses and not-for-profits will again need to demonstrate that their actual GST turnover has significantly fallen in each of the June, September and December 2020 quarters relative to comparable periods (generally the corresponding quarters in 2019).

The Commissioner of Taxation will have discretion to set out alternative tests that would establish eligibility in specific circumstances where it is not appropriate to compare actual turnover in a quarter in 2020 with actual turnover in a quarter in 2019, in line with the Commissioner’s existing discretion

Eligible Employees

The eligibility rules for employees remain unchanged.

Only one employer can claim the JobKeeper Payment in respect of an employee.

The self‐employed will be eligible to receive the JobKeeper Payment where they meet the relevant turnover test, and are not a permanent employee of another employer.

Employees will continue to receive the JobKeeper Payment through their employer during the period of the extension if they and their employer are eligible and their employer is claiming the JobKeeper Payment. However, the amount of the JobKeeper Payment will change at the rates set out above.

The chart below provides a quick overview of the JobKeeper 2.0 Payments

Need our Help?

If you would like our assistance assessing the criteria, eligibility or applying for the JobKeeper extension package and/or other Government stimulus packages, please contact our office to discuss our fees for this service.